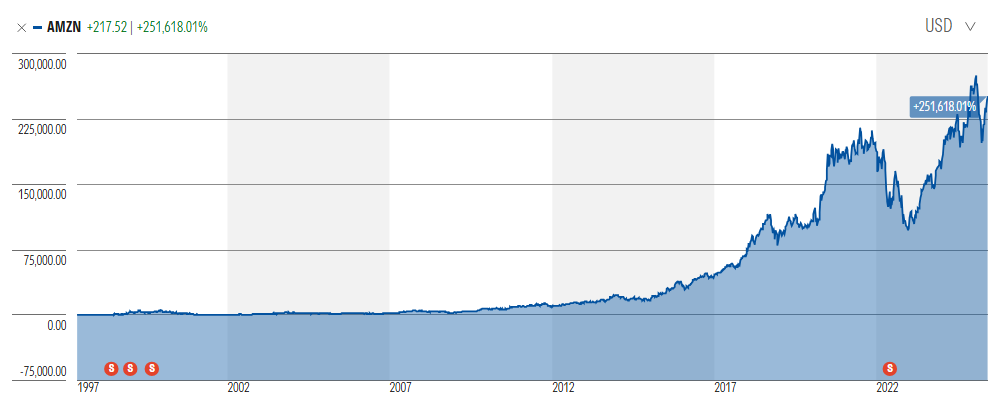

Amazon's Amazing 251,681% Return Explained

And what it would have taken to get it.

It all began on May 15, 1997.

This was the day the to-be universalist retailer Amazon.com (AMZN) hit the securities market as a publicly traded company — the shares floated at $18 each.

Though a mere embryo of the enterprise we know today, Amazon’s public debut was, nevertheless, an anticipated affair, with a horde of panting investors queued to bid up the price at the opening bell. And bid they did, and then some.

A year onward, the shares had risen to the point the Amazon’s board of directors thought a two-for-one stock split was in order. The ascent progressed unabated. Seven months after the first split, the board approved another split — this one three for one. The shares continued to defy gravity, and another split — two for one again — occurred nine months after the second split.

Let’s assume you were there. You were huddled amongst the crowd at the launch, and just as the engines were ignited, you bought 100 Amazon shares at $18 each (unlikely for a little ole retail investor, but humor me anyway). You then stepped down, sat back, and watched as your investment made for the wide blue yonder.

And if you did no more than sit and watch, good for you. Inertia paid off in spades. Eighteen months onward, your Amazon investment was valued at $110,000. A few months further afield and a few weeks shy of the two-year IPO university, your investment — now counting 1,200 shares after the three stock splits — had ballooned to over $126,000.

Human nature is an odd concoction, though. Most investors would be luxuriating in their good fortune. You, on the other hand, were given to episodes of self-reproving when you reflected on the windfall. Why not more? The kids’ college fund could have been liquidated, the house could have been further mortgaged, the missus’s engagement ring could have been pawned at that payday lender on the sketchy side of town. You knew Amazon was a winner, and you’re annoyed for having played it too safe.

Oh well, what you lacked in audacity, you were compensated for with unwavering equanimity and a Jobian capacity for patience. You kept your head down, oblivious to the market vicissitudes. You neither added to nor subtracted from your original stake. All changes in value were exogenous.

And here you are twenty-eight years later in 2025. You no longer own 100 Amazon shares; you no longer own 1,200 shares. After the twenty-for-one split in June 2022, you now own 24,000 shares. Your 24,000 shares are worth $5.2 million (approximately) today. Your annualized compounded return was 32% over your twenty-eight-year holding period. Your investment generated a 218,618% stem-to-stern return. (The S&P 500 with dividend reinvestment generated a 9% annualized return and a 1,083% total return over the same period.)

It happened, but is it plausible or even possible?

The empirical evidence confirms it’s possible, but so is it possible that someone would marry Scarlett Johansson, win the Monaco Grand Prix, and formulate the first large-language AI model. Plausibility is a separate consideration. We should be careful not to conflate the two. I could have married Scarlett Johansson, won the Monaco Grand Prix, and formulated the first large-language model. I’ll leave it to you to infer if such feats were plausible. I hope you inferred correctly.

Perhaps an investor exists who resolutely held his Amazon shares over the past twenty-eight years. We naturally assume one person has, but our assumption proves wrong.

Amazon founder, current board chairman, former CEO, and occasional rag-sheet gossip fodder Jeff Bezos has periodically reduced his Amazon stake over the years, with the number of shares sold and the amount of the proceeds received rising over the past ten years. His February 2022 sale of 50 million Amazon shares valued at $8.5 billion is the largest to date. More sales are planned.

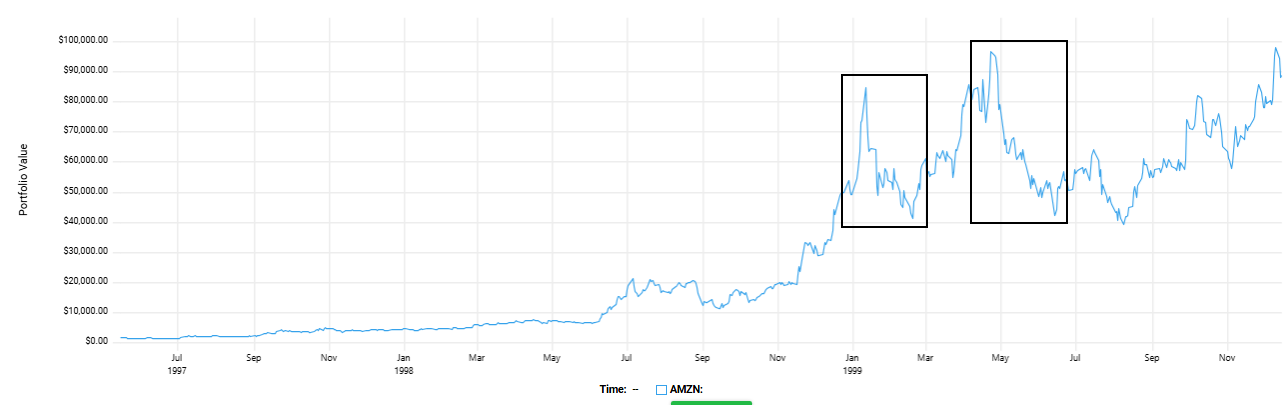

I doubt that most, if not all, investors who participated in the 1997 IPO persevered until the end of the 1990s, much less 2025, without selling some, if not all their Amazon shares. The long-term trajectory has been onward and upward, to be sure, but the trajectory has hardly been linear. Sudden and violent drawdowns have rattled equilibrium more than once. Two 50% drawdowns occurred in 1999 alone.

When times are good and stocks are persistently rising, investors will chest-puff and fortify a swelling intrepidity with useless platitudes, such as the Rothschild-inspired “buy when there’s blood in the street” or the Buffett quote “be greedy when others are fearful and fearful when others are greedy.” This is simply human nature doing its thing once again: We exaggerate our pain tolerance when pain is nonexistent.

The problem is that blood in the street is evidence of something dying, and many an internet stock suffered an unstanchable bloodletting a few months into the 2000s. As for Buffett’s contrarian observation, most of us fail to recognize who’s greedy and who’s fearful. Investors are reluctant to sell into a raging bull market and to buy after into the savagery of a mauling bear market. As much as we like to paint ourselves as the stoic individualist, we are mostly inclined to integrate with the herd. If we are unable to recognize greed and fear in ourselves, how can we recognize it in others?

Inappropriate anchoring further erodes resolve. When an $1,800 cost-basis investment ascends at a sixty-degree angle to $110,000, the cost basis is forgotten. The $110,000 assumes the role of reference point. When $110,000 is cleared by a sufficient margin, and $126,000 suggests the clearing of a sufficient margin, it, too, is supplanted in the memory bank. Both highs were succeeded by a punishing share-price plunge.

Six weeks after the $110,000 high, your Amazon investment had dropped to $54,000. Amazon shares reversed course, throttled up to full power again, and shot to a new high. Two months later, your portfolio was valued at $126,000. With all deference and respect to Mark Twain, history not only rhymes, it repeats. Another hard sell — one harder than the first — followed and two months after the euphoria of the new high, your Amazon investment was again valued in the mid-$50s.

Fissures began to appear.

The irrational exuberance that dominated the 1990s internet revolution subsided into a general uneasiness as we entered 2000. Uneasiness digressed to concern; concern yielded to panic. A punishing, protracted pay-the-piper recession ensued that ended two years later with the S&P 500 enduring a 48% max. drawdown, which is almost merciful when compared to the 83% beat-down experienced by the tech/internet-dominated NASDAQ 100.

As for that $1,800 investment that had breached $126,000, it had been reduced to $7,200 at the worst of it. You’re still far ahead with $7,200 arising from an $1,800 investment, but the peak-to-trough max. drawdown was 94%. “Woulda, coulda, shoulda,” was a recurring lament for many investors in the early 2000s.

The correction was inevitable in hindsight because everything in hindsight is inevitable. Companies that were little more than a webpage and a cutesy mascot were floated and valued in the hundreds of millions of dollars (boo.com, etoys, webvan). I remember the era well. Forget valuing a company on silly old metrics like revenue and cash flow. Clicks and click-throughs are what mattered.

(Sidebar: In 1999, Mark Cuban and his business partners achieved billionaire status by selling a laughably lipsticked internet pig to Yahoo! for $5.7 billion. Cuban and his pals started and sold Broadcast.com to Yahoo! In 1998, Broadcast was estimated to have reported $22 million in revenue, which generated a $16.4 million loss. Yahoo! saw value that evaded most sentient people. Cuban received a billion dollars’ worth of Yahoo! stock for his Broadcast.com position. He immediately locked in the value with a sophisticated option trade to get him to the lock-up expiration. Here, we see asymmetrical knowledge at work. Yahoo! eventually acknowledged what Cuban must have known. Yahoo! closed Broadcast.com and wrote off the $5.7 billion in full in 2002.)

Amazon was different. It was growing revenue but also losses during the formative years. The first reported per-share profit didn’t arrive until the fourth quarter of 2003 — six and a half years after the public debut.

We should remember that in the early 2000s, Amazon was no dominating Goliath (and cloud services provider). It began life as an online bookstore, but there were others, namely Borders and Barnes & Noble. Bezos was alert enough to realize more than books were fair game for online retailing. Amazon was soon selling music, DVDs, computer software and hardware, but it was still unrecognizable as the Amazon we frequent today.

A Little Avuncular Insight

Ignore the big-number seduction. You could have invested $1,800 to generate a 251,681% return, as I could have married Scarlett Johansson, won the Monaco Grand Prix, and formulated the first large-language model. Technically, they were possible; practically, they were impossible, so they should be dismissed. Hope springs eternal. If it were otherwise, lotteries would never exist.

The potential to realize instant generational wealth is pitched most during seismic technological shifts: railroads, telegraphs, electrification, automobiles, air travel, computers, internet, and now artificial intelligence. Act early and act fast and you could be the next investor boasting about a two-hundred-thousand-whatever percent Amazon-like return. The far greater probability that you’ll end up hiding in shame because you rode the next equivalent of webvan or boo.com to zero. Pioneers are known to get slaughtered.

I’ve been investing professionally and personally for over thirty-five years (closing in on forty). Investing is occasionally frustrating, confounding, and always boring if done correctly. Investing should arouse little emotion. For that reason, I find that fund investments — mutual, exchange-traded, and closed-end — are more conducive than most investments to ensuring equanimity. The highest probability of long-term success occurs when accumulating 11%, 12%, or 13% average annual returns while minimizing volatility.

(Sidebar: I give high preference to a few fund metrics: CAGR, max. drawdown, daily volatility, and the Sharpe and Sortino ratios. CAGR reveals the historical average return. The other four express volatility (risk). The higher the CAGR and Sharpe and Sortino ratios and the lower the max. drawdown and daily volatility the better. I never consider return without considering the other metrics.)

Naive investors will see Amazon’s spectacular 28-year total return and imagine a linear ascent up a very steep incline. I hope I’ve disabused you of the false perception. The journey more often resembles the flight path of a butterfly. It can get you where you’re going, but the journey is everything except a straight line.

Investing consists of redundant daily seesawing — up one day, down the next, though, if done correctly, a little less down and a little more up over time — punctuated by the occasional huge move. Most of Amazon’s return was the product of a few “big-pop” days — when the stock surged on unexpected positive news. Eliminate these big-pop days, and you’ve eliminated the ostentatious return. I offer a personalized example.

I have owned Oracle shares for years. I’ve ignored Oracle most of the time. I’ve gone months without checking the stock price. When I do check, I’ll see a daily pattern of seesawing along an unpretentious incline. But something newsworthy occurs, and I will notice because the Wall Street Journal and Barron’s leave me no choice.

Oracle shares rallied 22% over the final two days of trading last week. The company reported consensus-beating quarterly financial numbers and an upbeat outlook on its future because of AI or something. (I’ve yet to delve into it.)

Was I excited? No, though I suppose that if the opposite had occurred, I would have been annoyed, but even that feeling would have proved fleeting (because I have experienced single-day hard sells on a disappointing quarterly outlook and tempered expectations). More often, I find myself pondering “Now what?” after a surge or a slump.

I own Oracle and most of my other stocks in a taxable account. Because I have owned Oracle for years (as I have owned the others), a sale would trip a long-term capital gains tax. I loathe paying taxes. Why should I sell Oracle? Because I fear the share price could retreat after such a large leap forward? It probably will, but so what? I worry little about the company’s business outlook. But if I did sell, what would I do with the proceeds? It’s an involved consideration.

I’m a Chartered Financial Analyst (CFA) and have been one for a few decades now. Most of my career has centered on analyzing and recommending individual securities. I spend most of my time in my professional career still plying the trade of individual security analysis. I think I know what I’m doing most of the time, which is no guarantee of getting it right.

On the home front, I began to shift gears about ten years ago. I have gradually reduced my holding of individual securities to a few legacy issues (like Oracle), which I expect to hang on to until the bitter end and let the next generation handle. My personal account is now populated mostly with fund investments. (I’m also in my sixties.) I realize I have only kicked the can down the road. Someone else is deciding when to buy and sell, but that’s OK because I have done my due diligence. I have vetted and bought funds run by managers with a similar investment style and attitude (more concentrated portfolios with low annual turnover) as mine.

The older I get, the more I appreciate this tortoise approach to investing: The grinding ahead out of habit, like brushing your teeth in the morning, and the lack of sensation and anticipation associated with the process. Investing registers in my mind as something that needs to be done with no thought that it won’t be done. When I review the whole shebang and see aggregated appreciation (somewhere between 10% and 15% annually), I’m satisfied. If not, there’s always next year.

I’ve long ago inured myself to pitches that promise to “turn $5,000 into $100,000” or how to “10x, 20x, or 30x” my money. The pitches aren’t necessarily wrong: the S&P 500 will 10x your money and turn $5,000 into $100,000 if given sufficient time, with time being the crucial variable. Tell someone you can double his money in five months and watch his eyes alight. Tell someone you can double his money in five years and listen to the groan of disappointment.

(Sidebar: You will also frequently find investment pitches centered on “total addressable market,” which refers to the total revenue generated by the participants in a particular sector. For instance, the energy market in total might generate $20 trillion in annual revenue. The number is a loose estimate of all the participants — drillers, refiners, retailers, explorers, transporters, etc. — total revenue. The estimate can be predicated on current market revenue or future market expectations. AI is ripe for such pitches because any figure we apply to “total addressable market” is unfalsifiable. No one knows, so why not fabricate an outlandish estimate and hitch a wagon to it? Ponder the potential: If a newbie company with $10 million in annual revenue can capture only 0.05% of a $20 trillion total addressable market, the sky is the limit. Do tread carefully when confronted with pitches like this and this.)

NOW FOR THE BOLD-FONT FINE PRINT: The text above should not be construed as investment advice. It is neither a solicitation for nor recommendation of any security or investment mentioned. It is information only. I have opinions. What works for me might not work for you. Always remember the buck stops (and starts) with you, and you know you better than anyone. or at least you should.

DISCLAIMER: THE AUTHOR DOES NOT GUARANTEE THE ACCURACY OR COMPLETENESS OF THE INFORMATION PROVIDED ON THIS PAGE. THE INFORMATION CONTAINED ON THIS PAGE IS NOT AND SHOULD NOT BE CONSTRUED AS INVESTMENT ADVICE AND DOES NOT PURPORT TO BE AND DOES NOT EXPRESS ANY OPINION AS TO THE PRICE AT WHICH THE SECURITIES OF ANY COMPANY MAY TRADE AT ANY TIME. THE INFORMATION AND OPINIONS PROVIDED HEREIN SHOULD NOT BE TAKEN AS SPECIFIC ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. INVESTORS SHOULD MAKE THEIR INVESTIGATION AND DECISIONS REGARDING THE PROSPECTS OF ANY COMPANY DISCUSSED HEREIN BASED ON SUCH INVESTORS’ REVIEW OF PUBLICLY AVAILABLE INFORMATION AND SHOULD NOT RELY ON THE INFORMATION CONTAINED HEREIN.